Question from a buyer - seller concessions

What are they? Why would I want them?

I had a buyer today asking me about adding seller concessions into his purchase offer so I thought I'd run through an explanation of what they are.

When you buy a house, you need "cash to close".

Cash to close is a term that includes 1) the down payment on the house - this will be your equity in the house to start. So if the house costs $200,000 and you have a 5% down payment = $10,000, this means you have $10,000 in equity and owe $190,000 on your mortgage.

Cash to close also includes 2) additional costs - money that you pay the lender for the mortgage. It includes fees (which banks are famous for), the appraisal, sometimes mortgage points, attorney fees for the bank, title insurance to cover the bank etc.

The buyer who was asking me about seller concessions today had been quoted an additional $6,600 in closing costs he would have to come up with (above and beyond his down payment). He doesn't have that much. So now what do we do?

One solution is to finance the $6,600 closing costs by adding it to the mortgage. This can be an inexpensive way to finance that money because, as we all know, interest rates are super low right now!

The way this works is like this: We take the purchase price of the house, let's use the $200,000 example again. Your contract looked something like this without seller concessions:

purchase price of house $200,000 the amount the seller has agreed to sell the house for

down payment $ 10,000 this is your 5% down payment (in this example)

due at closing $190,000 this is the amount the bank is loaning you for the house

but... you also need $6,600 in closing costs....

With seller concessions of $6,600, you are borrowing the money for closing costs.

Your contract will look a little more like this now:

purchase price of house $206,600 the seller's $200,000 plus $6,600 closing costs

down payment $ 10,000 your 5% down payment (in this example)

due at closing $196,600 the amount the bank is loaning you for the house AND your closing costs. Of this $196,600, the seller gets $190,000 same as above, and you get $6,600 back - which is why a seller concession is also sometimes called a "seller give-back".

Of course, you then immediately turn around and use that $6,600 to pay the bank the fees you incurred for the mortgage so you don't get to enjoy it, but you DO get to enjoy your new home!!

Hope that makes understanding SELLER CONCESSIONS a little easier and as always, if you have any other questions I can answer, please let me know!!

Maria

518-857-6396

www.MariaBarr.com

Open House today Feb 9 noon - 2pm

51 Woodcrest Drive, Glenville $229,900

4 bedrooms, 2 baths, 1824 sq ft plus FULL walkout basement

call me if you have questions:

Maria Barr

(518)857-6396 or email mbarr@realtyusa.com

I'm holding open 51 Woodcrest Drive in Glenville today. This awesomely maintained home is in the Niskayuna school district but has low Glenville taxes. Some of the reasons you'll want to see it are:

- recently remodeled and upgraded kitchen with granite and stainless

- hardwood floors

- huge livingroom

- family room w fireplace

- 2 full baths

- full walk out basement

- 2 car garage

- terrific yard

- deck

There are lots more pluses, come check it out.

Contingencies Your Offer Should Include - The Structural Inspection

Use contingencies as a safety net when buying or selling your home.

In this series, I talk about the contingencies found in a typical real estate purchase and sale agreement. Today, I’ll be discussing the STRUCTURAL INSPECTION contingency. It’s typically the second contingency date on the real estate sales contract time line. Normally, and I recommend this is always the case -especially for buyers, it overlaps and extends beyond the attorney approval period (see my blog on the attorney approval period at www.Maria Barr.com).

A typical time period for the structural inspection is 2 weeks. It makes sense to schedule your inspections as soon as you negotiate your contract. Schedule them for as soon as possible after your attorney approval date. Keep in mind we need to allow enough time for test results to come back from the lab (water, radon).

In rural locations, a septic inspection may need to be scheduled separately. Home inspectors can do a dye test for the leach fields but are not able to visually inspect the tank, you need a septic company to do this. (Don’t worry, your agent will help set up inspections if you need assistance!)

The structural inspection contingency allows buyers to re-evaluate their situation should “a SINGLE defect that would reasonably cost in excess of $1,500 to remedy” be found. Which means: if the roof needs to be replaced and would cost over $1,500 this contingency would kick in. A laundry list of small items addingup to $1,500 does not qualify.

A DEFECT OVER $1,500 IS FOUND...

What are the buyer’s options at this point?

1. The buyer may cancel the contract if he chooses.

2. The buyer may negotiate the repair by asking the seller to pay for some or all of it.

3. The buyer may decide to move forward with the purchase in spite of the problem.

What are the seller’s options?

1. If the buyer cancels the contract, the seller may put the house back on the market as it was or after performing the repair. The property disclosure must be updated to reflect the new information.

2. The seller can agree to negotiate, or may refuse to negotiate. Ask your agent for their advice, she will have a perspective on how long it may take to find another buyer if this contract falls apart.

Next time, I’ll be talking about the mortgage contingency. These are just the basics, every transaction is unique and you may find yourself faced with some situations not covered. Please feel free to contact me directly if I can help with any questions.

-Maria

www.MariaBarr.com

Contingencies Your Offer Should Include - The Attorney Approval Period

Use contingencies as a safety net when buying or selling your home

You've found the home you picture yourself living in and now you're ready for the next step - making an offer. Today I'm going to talk about one of the standard contingencies to a purchase contract. - the attorney approval period.

These contingencies are designed to protect the parties to the contract, namely buyer and seller, by detailing conditions that must be met before the closing will take place. In this series, I'll be covering them in chronological order (for the typical transaction), starting with the attorney approval period.

The attorney approval period is typically between 3 and 7 days, although it can be longer. I counsel my clients so they understand that during this contingency period, the contract can be cancelled by either party for any reason. If the contract is cancelled during the contingency period, the contract deposit (also called earnest money deposit) is returned to the buyer, under normal circumstances.

So, imagine this sellers. We have a 5 day attorney approval date and your buyer gets cold feet on day 3. Their attorney can cancel the contract by notice to your attorney and they will receive their deposit back. I counsel sellers to wait out this time period before making any potentially costly decisions - like putting a deposit on a moving truck etc.

And you buyers out there, if the seller gets a better offer on day 4, they can cancel your contract and go with the higher offer. You will usually be given the opportunity to improve your offer, but not always. The seller is not morally or legally required to stay in the contract during this period so please, make sure your dates match your needs!

An important strategy for buyers and sellers is to set the length of this contingency period according to current market conditions. As an example, if you are buying and there's a lot of competition, set the date short - 3 days. You'll have less exposure to being bumped by a better offer.

For either party, I recommend ensuring the other contingency dates are consistent with the attorney approval date. One example - as a buyer, you don't want to find yourself having to pay for a structural inspection before the attorney approval date because the seller can still cancel the contract and you will be out the expense of the inspection.

The attorney approval period can feel like limbo, but you'll find the rest of the time before your closing goes by very quickly!

Next time, I'll be discussing the structural inspection contingency. Please feel free to comment or email me directly if I can answer any questions.

-Maria

www.MariaBarr.com

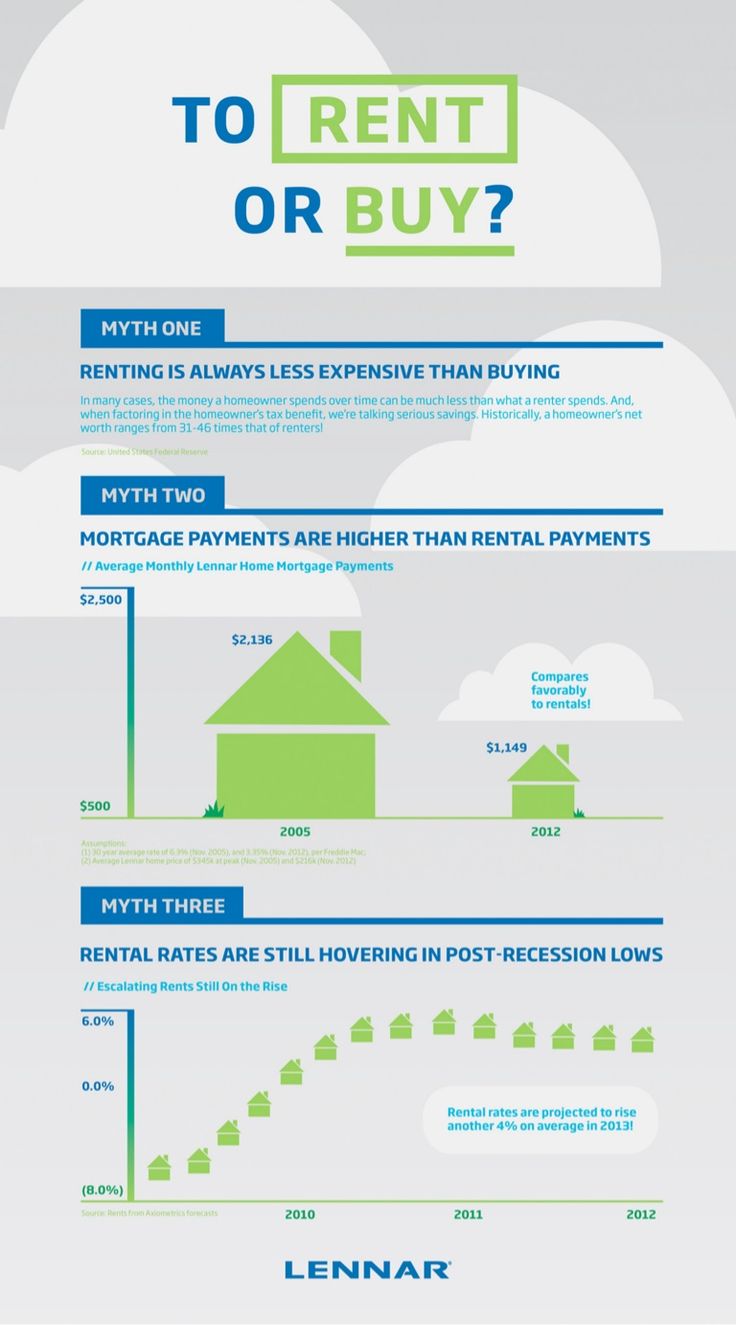

Some food for thought..

Looks like a bit of home investment might be more favorable than you'd expect! Interesting!